Sensing the Supercycle: $VPG

Running back the AI Playbook for the Robotics Era

Vishay Precision Group VPG 0.00%↑ is no longer a boring, stagnant industrial cyclical. It has quietly become a primary bottleneck (I know it’s such a buzz word now, shoot me) for the most ambitious hardware project in human history: the mass deployment of humanoid robots. While the market is manic on the data center buildout, the physical world requires a nervous system to translate digital intent into mechanical action. $VPG owns the proprietary foil technology that makes this translation possible and is designed into Figure’s and Optimus’ production-ready robots. The Physical AI trade will be where the puck moves next and I am positioned to be earlier than the masses.

As of May 5, 2026, Vishay Precision Group trades at a ~$850M market cap. The equity remains fundamentally mispriced relative to its role as a tier-1 supplier for the humanoid revolution.

VPG High-Level Overview and Vertical Positioning

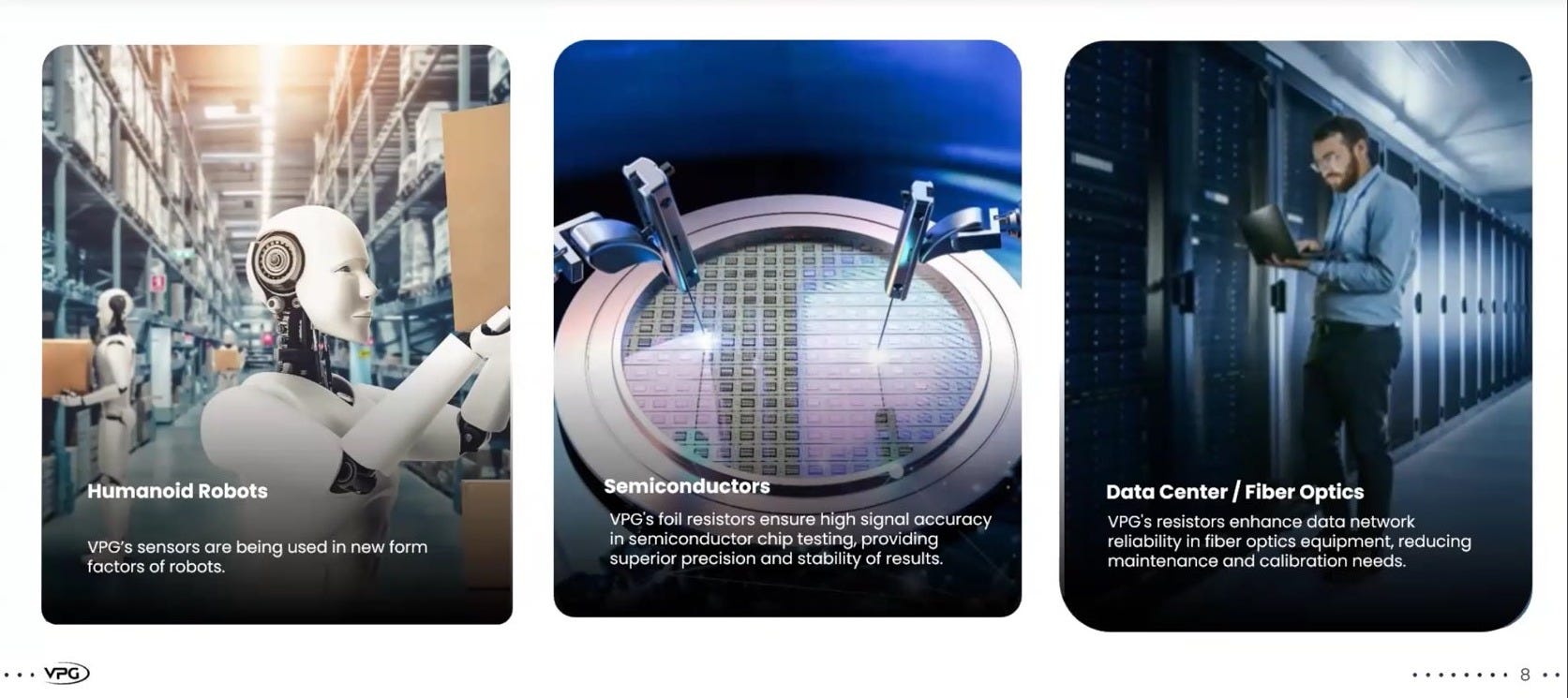

Vishay Precision Group operates at the critical intersection of physical AI and precision measurement. The company specializes in foil strain gauge technology, which serves as the nervous system for advanced robotics. This technology allows machines to perceive force, weight, and torque with human-like sensitivity. $VPG is currently positioning itself within key high-growth verticals: humanoid robotics, broader physical AI, fiber optics for data centers, semiconductor testing, and aerospace/defense sensors.

The company has successfully transitioned from an engineering partner to a production-scale supplier for top-tier robotics firms. Beyond robotics, $VPG is securing material orders from a leading laser manufacturer, like Lumentum, for precision resistors to support the infrastructure requirements of the agentic AI era. These precision resistors are mission-critical for maintaining laser performance in data centers where high-speed data transmission is paramount. They are also in discussions with multiple players in the broader Physical AI space, like autonomous logistics.

The most significant near-term catalyst is the upcoming Q1 2026 earnings call and humanoid order updates, where management is expected to unveil refreshed 3–5 year financial targets. I foresee management will provide conservative targets of high teens revenue growth, 45% gross margins, and 20-22% operating margins.

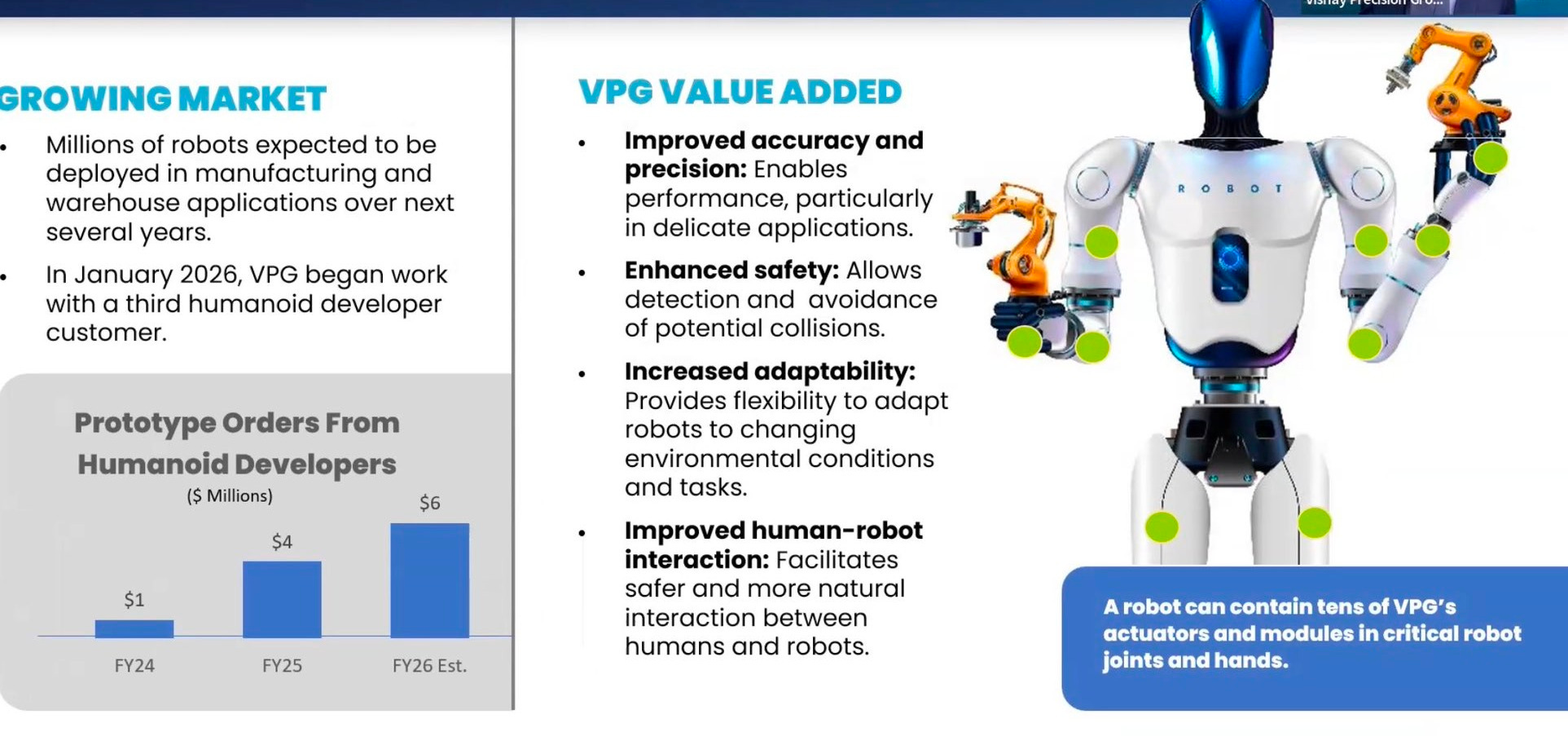

$VPG shattered its $30M business development (BD) target for 2025, delivering nearly $38M in actual orders. For 2026, they have set a $45M BD target. This figure is a conservative floor because it only includes a $6M humanoid revenue estimate. Vishay also closed a third humanoid customer in Q4 that is currently in the design phase. Management is being overly cautious on humanoid timing to avoid jumping the gun on the ramp. While this is ultimately a humanoid story, the other growth levers—specifically optical laser resistors, other Physical AI opportunities, and aerospace sensors—are poised to provide serious upside optionality that the market is currently ignoring.

McKinsey Believes Sensing is the Bottleneck

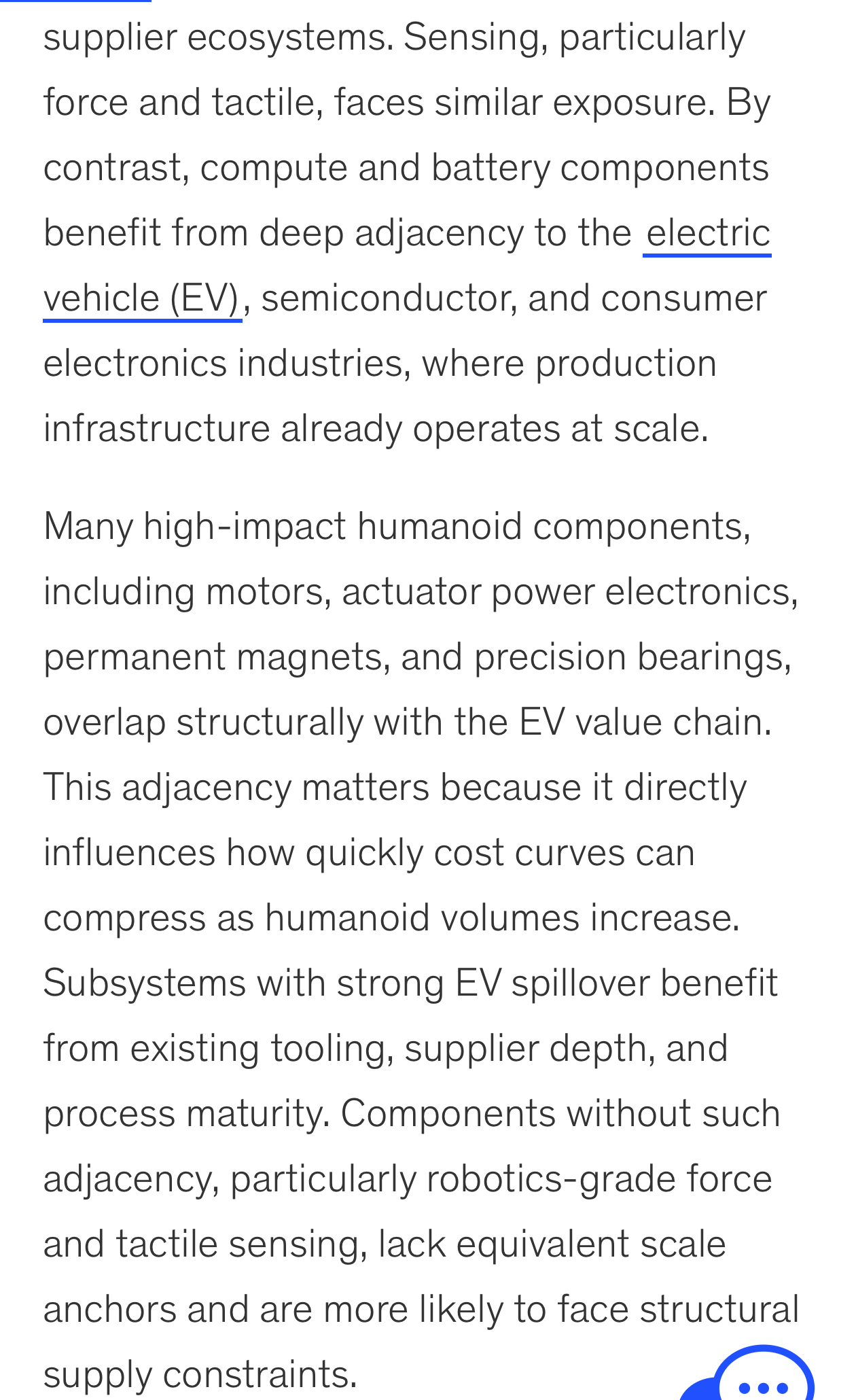

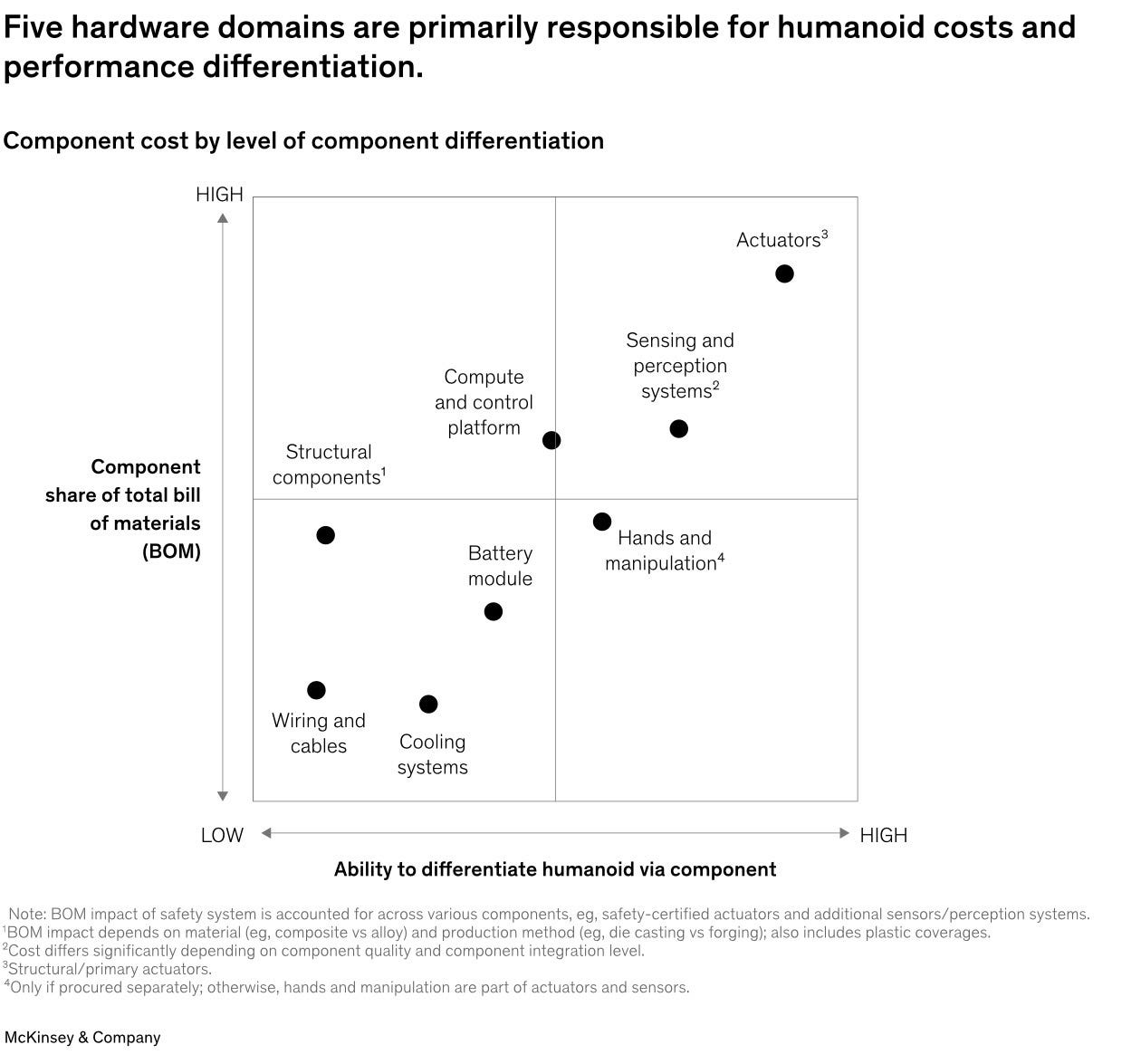

A recent McKinsey report, “Turning humanoid supply chain constraints into billion-dollar wins,” highlights a critical divergence in the robotics bill of materials (BOM). While components like batteries and motors benefit from massive electric vehicle (EV) economies of scale, robotics-grade sensing lacks a standardized, high-volume anchor.

McKinsey’s matrix identifies components that drive both high BOM share and high component differentiation. VPG sits in the upper right quadrant: High Share of Humanoid BOM and High Level of Component Differentiation.

Precision sensing is the primary differentiator for dexterity. For humanoids to move from laboratory curiosity to factory labor, they require sub-gram sensitivity and zero-drift thermal stability. $VPG is the only company providing this at a transducer-class level. Most components in a humanoid benefit from automotive spillover, but six-axis force/torque and tactile sensors do not. This makes $VPG a sole-source bottleneck provider for the industry and is the only pure-play humanoid supply chain stock under a $1B market cap, and they just so happen to be designed into the two leading humanoid manufacturers in the USA…

Customer 1: Tesla Optimus

The relationship with Customer 1 is the foundational pillar of the $VPG investment thesis. While not explicitly named in filings, the technical specifications and production timelines point directly to Tesla ($TSLA). This connection was further bolstered by a $VPG holiday campaign visual that featured an Optimus Gen 2 interacting with delicate objects.

Here are key dots connected:

Design Win: VPG officially announced a significant design win with a leading humanoid developer (Customer 1) in November 2023. At the time, management noted the project was in the “beta phase.”

Design Phase: VPG has indicated they have worked with this customer since 2022, aligning with Tesla Optimus beta timelines.

The Unveiling: Just weeks later, in December 2023, Tesla unveiled the Optimus Gen 2, which featured the exact advanced tactile and force/torque sensors that are VPG’s core specialty.

Production Alignment: By the August 2024 earnings call, management stated their customer planned to deploy “thousands of robots internally” by the end of 2025, which perfectly matched Elon Musk’s publicly stated timeline for Tesla’s internal rollout.

Here are the key facts to know about the Tesla relationship:

Hardware Integration: $VPG supplies 15 to 20 torque sensors for each Optimus unit. These sensors are molecularly bonded to the actuators in the joints.

Manufacturing Scale: Tesla is currently re-tooling the Fremont factory for volume production. This site has a theoretical capacity of 1M Optimus units annually.

The Texas Expansion: The opening of Giga Texas in the summer of 2027 is designed to support an annual output of 10M Optimus units.

Production Velocity: $VPG management noted at the Sidoti conference that Customer 1 expects to scale to hundreds of robots per week by the end of 2026. This timeline aligns perfectly with the Optimus Gen 3 rollout.

Customer 2: Figure AI

The partnership with Customer 2 highlights VPG’s superiority in high-dexterity tactile sensing. This relationship correlates directly with the development at Figure AI.

Here are the key dots connected:

Design Phase: It has been indicated that VPG has been in design phase with Customer 2 since 2023.

Initial Orders: Customer 2 placed orders for the initial tactile sensor baseline pre-Q2 2025.

Prototype Ramp: In October 2025, VPG received a $600k follow-on prototype order just before the official unveiling of Figure 03.

Here are the key facts to know about the Figure relationship:

Fingertip Sensitivity: Figure requires 3-gram pressure sensitivity for the Helix 2 robot to function effectively. $VPG provides 10 tactile sensors per robot to enable this human-like touch.

The Invisible ASP Driver: As Figure moves toward higher degrees of freedom (DoF) in robotic hands, the sensor density per unit is expected to increase. We anticipate that a shift to 22 DoF architectures will significantly expand the revenue per hand, providing a powerful tailwind to VPG’s average revenue per unit.

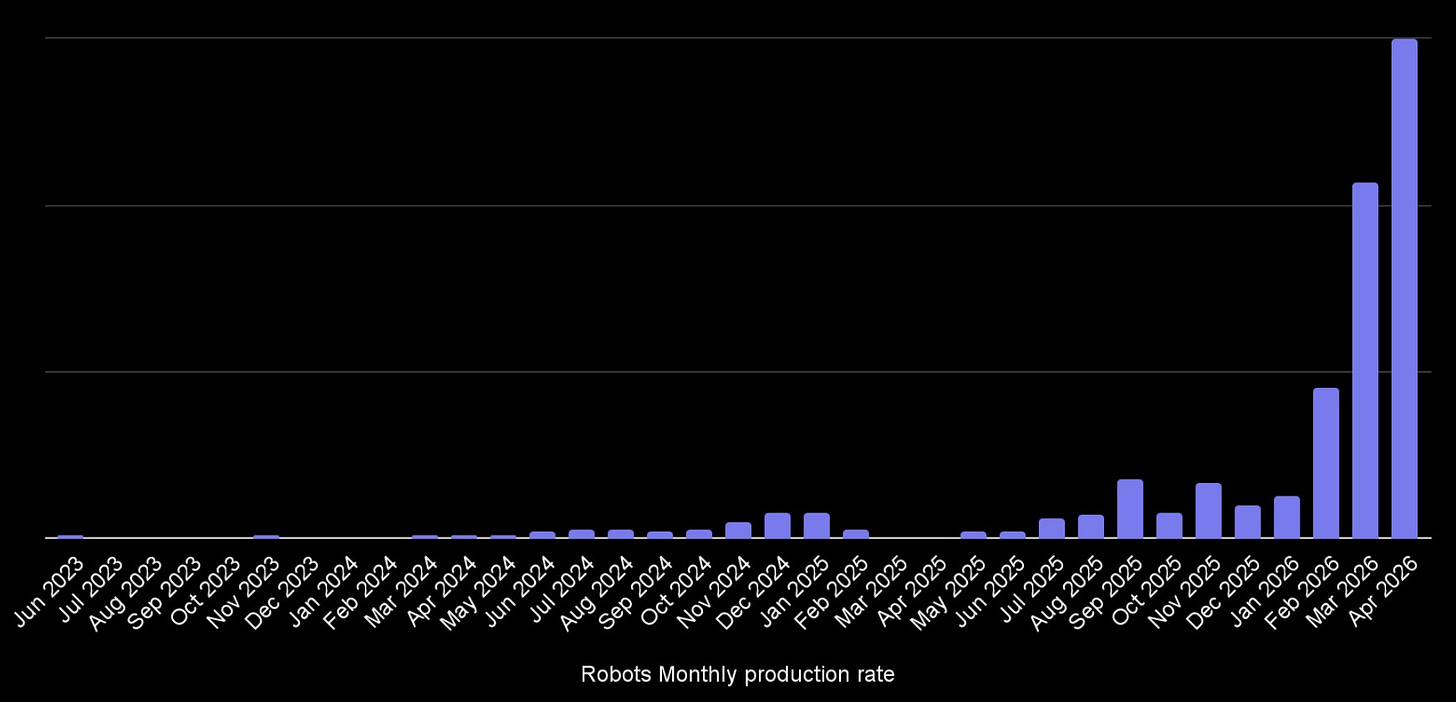

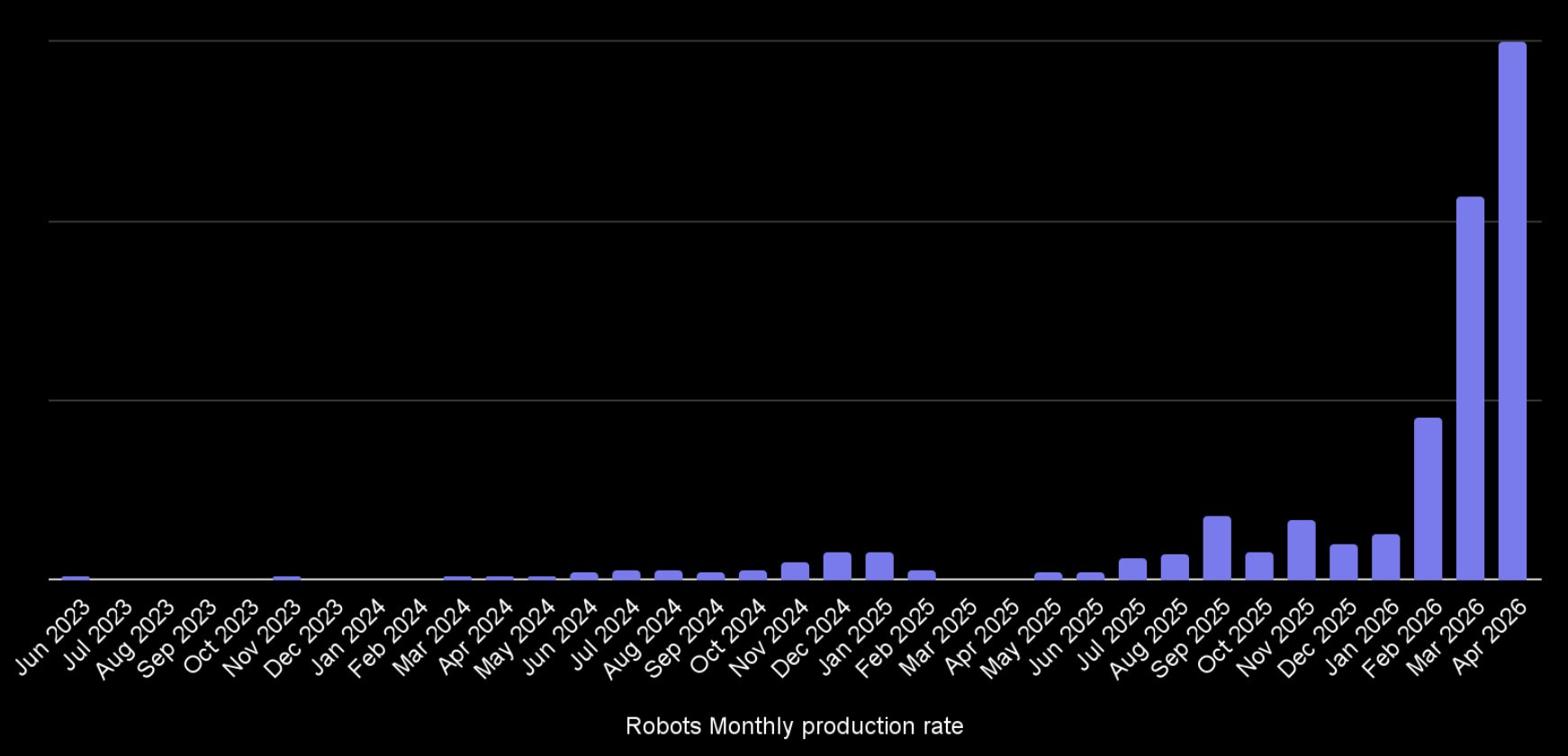

The Manufacturing Ramp: Figure has executed an aggressive ramp, moving from a near zero run rate in January to a ~3,300+ annual run rate as of April 2026.

Image provided by Figure CEO Adcock

Industry Leading Hand: Figure’s presentations have demonstrated incredible tactile sensing capabilities and dexterity, which both look to be industry leading.

Paraphrased: “Absolutely, most definitely, Customers 1 and 2 are top-five Western Humanoid OEMs. If I said their names, you would know them immediately.”

— VPG IR

The Strategic Moat: Why VPG Sensors Are Sticky

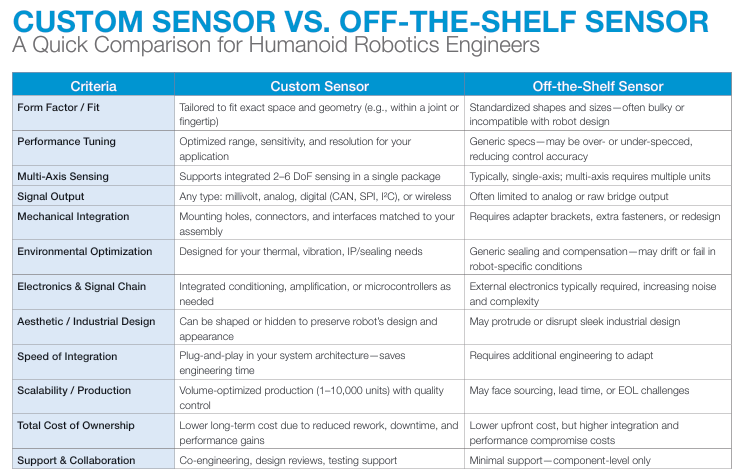

The hardware moat for Vishay Precision Group is becoming undeniably defensible. The stickiness of these sensors is a consequence of deep technical integration and high switching costs.

1. Data Lock-In and Neural Training

Tesla and Figure train their neural networks on the specific physics, noise profiles, and latency of $VPG sensors. These sensors feature a natural frequency of 98 kHz, which allows for near-instant response times. Switching to a different sensor provider would require these OEMs to re-collect a massive volume of training data. Ripping out the nervous system at this stage would cause significant delays and model drift.

2. Proprietary Metallurgy and IP

Torque sensors in robotic joints must endure massive heat from actuators without losing precision. $VPG uses proprietary foil alloys that maintain stability across extreme temperature gradients. This represents 60 years of metallurgical trade secrets. Competitors cannot easily replicate the recipe for these temperature-independent foils.

3. Safety Standards and Regulatory Necessity

In a humanoid meant for 24/7 labor, a sensor failure is a catastrophic event. $VPG sensors are transducer-class components designed to last the entire lifecycle of the robot. As safety standards for human-robot interaction become more stringent, the precision of $VPG becomes a regulatory requirement rather than an option.

Physical AI: An Adjacent Market Expansion

Beyond humanoids, $VPG is engaging with two large manufacturers on autonomous logistics applications. This represents the broader Physical AI umbrella, where autonomous systems require precise real-world data collection to navigate manufacturing and warehouse environments. Management views this as a 3-to-5-year roadmap that could become a meaningful driver of revenue as the nervous system requirement expands to all high-stakes automation. God knows how big this could become, but $VPG’s IR was quite excited when talking about the prospects across the Physical AI market.

Core Business Safety Net and 2026 Catalysts

Traders often overlook the core business, which generates over $300M in annual revenue. This segment provides a profitable floor for the stock. We have left the growth objectives of this core business out of our humanoid modeling, representing significant unmodeled upside and a strong floor for the stock price.

The primary catalyst for a valuation re-rate is the upcoming release of new 3-to-5-year financial targets and humanoid order updates. Management has stated that the infrastructure and supply chain are already built to support the humanoid ramp and they will not be the bottleneck. Consequently, most of the gross profit from this segment will flow directly to the bottom line due to minimal incremental SG&A requirements. We also hope to see gross margin expansion in the humanoid sensor business as the company identifies manufacturing efficiencies at scale.

Humanoid Revenue and Valuation Modeling

Our modeling assumes that revenue per robot compresses as production scales. We assume a price of $850 per robot during prototyping, dropping to $600 at 200k units and $400 at 400k+ units. I am using the $400/unit at scale from my IR touchpoints discussing “Customer 1” revenue per unit. I am still unclear what revenue per unit looks like for “Customer 2” but am led to believe it could be higher than $400 at scale. This model assumes that revenue and unit volumes largely come from Customers 1 and 2 without any impact of their newest third customer in the design phase of their humanoid or any new potential customers that could come.

This modeling exercise is more to show the leverage VPG has to a humanoid hockey stick ramp and margin assumptions could be subject to change. I am possibly slightly overstating EBITDA flow in 2028/2029 and understating gross margin potential in 2029/2030 as manufacturing / supply chain efficiencies could be unlocked.

Base Case Scenario (35% GM / 30% EBITDA)

Bull Case Scenario (38% GM / 33% EBITDA)

If you believe that humanoids scale to hundreds of millions or billions of deployments, the numbers get nutty.

Conclusion: VPG Follows the AI Infrastructure Playbook

The re-rate of critical AI infrastructure components follows a predictable playbook. We have seen companies like Celestica ($CLS) and Coherent ($COHR) transform from a few billion MC laggards to $65B leaders as their role as Tier-1 AI suppliers became clear. Vishay Precision Group is currently being priced as a legacy industrial entity despite its status as a sole-source bottleneck for the humanoid industry. As the market begins to price the humanoid revenue ramp and the massive operating leverage inherent in the business model, we expect a rapid convergence toward our price targets. The core business, optical resistors, and aerospace sensors provide a robust safety margin, but the humanoid nervous system is the engine that will drive a 10x or greater return.

NFA, I am long in size from $45.

Thank you for sharing. If you want to discuss VPG with someone else who seems to be following the company closely, check his substack: https://mcarbo.substack.com/

You’ll find several posts about the company there.

About your valuations, you are using very generous multiples. Apart from that, the company will do well. Maybe it’s a bit early to get into it, but that’s just my opinion, I may be wrong.